The new pension freedom rules present unique opportunities and challenges to advisers. With most restrictions to pension access out the window, and the perception rightly or wrongly that annuities are poor value, clients will look up to their financial planners for guidance on how best to sustain their income in retirement. Advisers are expected to guide clients through the plethora of income options, model the likely impact of taking large lump sums from their retirement fund and mitigate chances of clients running out of money. Huge responsibility! Fear not, help is here!

Are Cashflow Planning Tools Fit For Purpose?

Traditionally, many financial planners use cashflow planning tools to model likely retirement outcomes. Most of these tools are deterministic in nature, relying on assumptions such as average annual returns, inflation and like expectancy. These tools are for the most part, time value of money calculation. I believe that these tools aren’t fit for purpose for modeling retirement outcomes. I have written before about how the combination of sequencing risk, volatility drag and reverse pound averaging (or what some have revered to as pond cost ravaging) which a direct result of client taking income from their portfolios, make deterministic cash-flow forecasting rather meaningless and for the most part, misleading.

Take volatility drag for instance, If a £100K portfolio falls 10% in the year 1 and rises back 10% in the following year, the portfolio should be back to the initial amount of £100K right? After all the average annualized return of 0%.? Well wrong! The portfolio fell by 10% in year 1, so you have £90K,. To get back to the initial value of £100K, you need the portfolio to grow at around 11%, not 10%. So the portfolio needs to work harder to get back up. If you add portfolio withdrawals to that equation, the portfolio needs to work even harder to avoid the risk of running out of money. The point is, using deterministic cashflow planning tools that assumes average annualized return ignores the impact of volatility drag, sequencing risk and pound cost ravaging.

I believe that we need better ways of modeling retirement outcomes and a greater understanding of safe withdrawal rates in retirement portfolios.

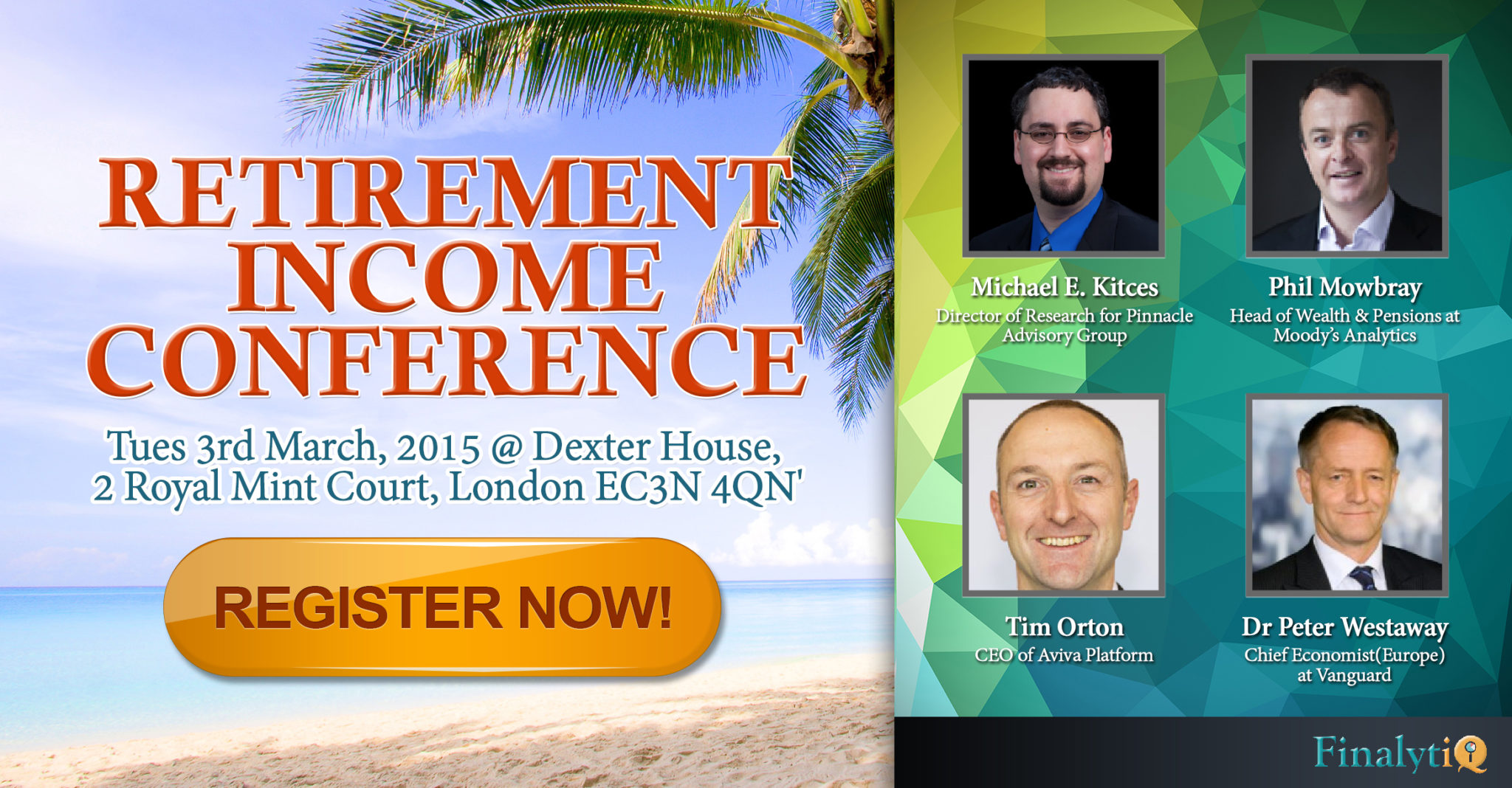

That’s why we’re putting together the Retirement Income Conference, to gives advisers practical insights and tools to navigate the uncertainties that face their clients in retirement. With leading experts drawn from the UK and the US, conference will demonstrate how latest research on safe withdrawal rates and the use of stochastic tool enables advisers to model retirement income options, demonstrate suitability and deliver better client outcomes.

I’m thrilled to welcome Michael Kitces, a highly regarded US-based financial planner, commentator and speaker, as one of our keynote speakers at this conference. While pension freedom is a new concept in the UK, retirees in the US have had virtually unrestricted access to their retirement fund for many years. I believe UK financial planners can learn a great deal from Michael’s experience. Michael will do a deep dive into the extensive research on safe withdrawal rates and how to establish sustainable retirement income for clients.

At the conference, Phil Mowbray, Head of Wealth & Pensions, Moody’s Analytics will offer practical insight on using of stochastic tools in cashflow planning; to assess risk capacity, demonstrate suitability and model retirement outcomes. His session will also demonstrate how to explain outcomes of stochastic model to clients in simply easy-to-understand language, without any of the industry jargon, while at the same time meeting regulatory requirements on suitability.

Another reason you do want to miss this conference is our tool of the Trade breakout sessions where advisers will get the chance to test drive a number of stochastic modeling tools and interact with the tool providers to get a first-hand experience.

Check out the conference page for details and registration.

Read Full Bio