For clients in retirement, developing a sensible and sustainable withdrawal strategy is at least as important as developing a sensible investment strategy. Unless a client annuitises all or most of their retirement pot, they need to have a robust framework in place to guide their withdrawal decisions or risk running out of money.

.

From April 2015, clients in pension drawdown will bid farewell to GAD rates (for the most part), and other restrictions on access to their pension funds. For many clients, the question simply will be – how much am I able to draw out of my pension pot without the risk of running out of money during my lifetime?

In 1994, US financial planner William Bengen famously postulated the 4 percent withdrawal rule using historical simulations. He would later coin the term “SAFEMAX” to describe the highest withdrawal rate, as a percentage of the initial account balance at retirement, which could be adjusted for inflation in each subsequent year and would allow for at least 30 years’ withdrawals during all the rolling historical periods in his dataset. He found that a first year withdrawal rate of 4%, followed by inflation-adjusted withdrawals in subsequent years, should be ‘safe’.

Some practitioners feel the 4% rule is rather naïve, as it ignores the dynamic nature of market and portfolio returns. More recent research has sought to determine the optimal withdrawal strategy by dynamically adjusting to market and portfolio conditions.

How would Bengen’s research have applied in a UK context? Luckily, in 2010, Wade Pfau replicated Bengen’s research in 17 developed countries including the UK. Pfau’s initial research used 109 years of financial market data (between 1900 and 2008) for the 17 developed market economies, using domestic asset classes and currencies. With this data, he used an historical simulations approach, considering the prospect of individuals retiring in each year of the historical period. Because of the assumed retirement duration of 30 years and the data ends in 2008, retirements take place between 1900 and 1979 – i.e. 80 retirement dates for each of 17 countries.

So what does the data tell us about safe withdrawal rates for UK retirees? Sadly it’s not good news.

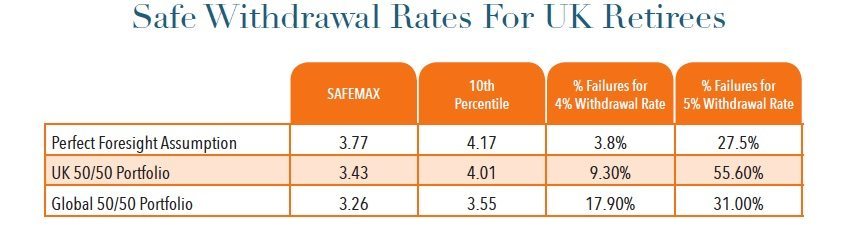

Pfau determined that even with perfect foresight of the best combination of UK equities and bonds (a concept that is unrealistic in real life), SAFEMAX for UK is 3.77%. If a client is prepared to accept a 10% probability of failure however, the SWR improves to 4.17%. At a 5% withdrawal rate however, the probability of failure is 27.5%.

Since the concept of perfect foresight is wishful thinking, Pfau’s results for a 50/50 portfolio puts SAFEMAX at 3.43%. But if a 10% probability of failure is acceptable, then the SWR is 4.01%. Interestingly, a withdrawal rate of 5% has a failure rate of a whopping 55.6%! Pfau later revisited the research to see if global diversification improves the SWR. He found that with a 50/50 portfolio the SAFEMAX is 3.26% and where a 10% failure rate is acceptable, the SWR rate is 3.55%. This indicates that the SWR actually worsened for UK retirees.

The table below summarises the findings:

Perhaps worryingly, Pfau’s research assumed fund charges and the adviser fee to be 0%. This is of course unrealistic, and if we were to deduct a conservative fee to account for the adviser fee, fund and platform charges, SWR for UK would be closer to 2% than 4%! (And around 3% for a 30% failure rate).

Join us at the Retirement Income Conference, where leading US financial planner Michael Kitces will explore latest research on Safe Withdrawal Rates in retirement portfolios.

Read Full Bio

Thanks for that Abraham, if they are basing it on safemax of 30 years, then do I assume we are working back from average life expectancy to a clients current age? Plus as there is the age old adage of “you can’t take it with you” how American and European property ownership compares to UK is probably relevant too as opting for equity release in LATER life, particularly for those with no children or spouse needs to be a consideration when calculating a safemax I would have thought? I highlighted LATER as whilst I have had the qualification for equity release since before it was mandatory I have only arranged 3 in 15 years as whilst I invariably explain it from an early age (late 50’s) I have had few I have needed to recommend it to (YET)

The SAFEMAX is not an answer to the retirement problem the majority of our clients face. It is only a result of a Monte Carlo simulation where the focus is on not running out of money when withdrawing from an investment portfolio.

Myself I am totally against the use of the Monte Carlo analysis and I prefer partial differential equations to describe the “retirement solution”. It is what I name the Methuselah equations.

However clients do not have only an investment portfolio, some of them have other important assets: main residence, buy to let properties, land, family businesses etc. Not to forget risk sharing arrangements between the members of the family (wife, children, parents) and social security arrangements.

There is another problem with the SAFEMAX which was brought to the attention of the Australian Government by a recent study; because of their risk aversion people do not spend enough from their earmarked retirement assets. It seems to be the result of too much risk aversion between retirees.

In UK we have also Inheritance tax, so there is a major tax incentive to spend some of your assets or gift them before dying. Not spending enough could be a higher risk than running out of money in retirement, so a line in the sand should be drawn somewhere.

I was always on the opinion that a financial planner should not separate the accumulation from the decumulation period, especially now more and more clients will phase their retirement. Good financial planning starts well before retirement, probably 20 years before, unfortunately the majority of retirees leave retirement saving for too late (last 5 to 10 years). The effect of the sequence return is a lot more riskier in accumulation than in decumulation (in decumulation at least you know you die one day, with or without any money left). In accumulation, the effect is that it does not allow you to retire, to do what you enjoy.

I did some research on a client of mine, where if he encounters a bad sequence of investment returns in the next 10 years, he will need to postpone retirement for up to 7 years. This guy really hates his job, although he is well paid so I am thinking to suggest some life planning coaching or therapy.

The assumption that retirees will spend the same at age 80 as they would at 65 needs to be challenged. As people get older they tend to spend less.