Annuity! That damn thing has been in the news a lot lately. There are people who think you should buy it, those who think you shouldn’t and then those who think you should sell the one you’ve got! Why do we love to hate our annuities so much? Why is it such an emotive subject?

The ‘debate’ (read bickering, talking over each other like school children) seems to be whether or not buying an annuity is ‘good value’. The trouble is that no one is asking the right questions, let alone giving any credible answers. Everybody has their own agenda – the Government has an election to win; the ‘industry’ (aka providers and sellers of annuities) clearly has vested interests and you’ll be safe to assume they are spitting out gibberish if you see their months moving! Then there are advisers – you lot aren’t saying much and if I didn’t know any better I’ll say you’re watching to see where all these end? And consumers? They really couldn’t give a monkey’s!

So what questions do I think we should be asking about annuities? I think we need ask some very basic questions that real people who buy an annuity would ask, like ‘how much money do I stand to make or loss on this thing?‘ What is the actual rate of return on a standard annuity? By that, I mean ‘internal rate of return’

You see, I emphasis that last point because if you ask the people who manufacture and sell annuities, even advisers and our very impressionable financial press what ‘annuity rates’ are, you get something like ‘it’s 5% for a 65 year old male.’ In fact, these figures are printed in the money section of your Saturday papers. It’s perfectly legal to do so. Trouble is, that’s not the whole truth. Not event close.

Why? Well, say I have £100K (which by the way I don’t in case you get the wrong idea) and I stick that money in a bank account that pays me 5% a year (humour me, please). That means I get £5,000 interest a year. I could go and splash out on booze, party like there’s no tomorrow, and may be buy the missus some red shoes or something! My £100K is still in the bank. Intact. That 5% is my ‘return.’ Got that? Good.

Welcome to Annuityland

You see, things don’t work that way in annuityland. If I hand over my £100K to an insurer and they offer to give me ‘5% a year’ on my annuity, technically speaking that £5,000 is a partial return on my original £100K. My £100K is no longer intact once I start taking that income. Under current rules, I couldn’t ask for it back, not for a standard annuity anyway. In fact, I wouldn’t start to making any ‘return’ until after 20 years when they have paid me back all my initial £100K. (i.e £5000 X 20). Only then, do I start getting any ‘return’ on my money. Trouble is Jim (or whatever your name is), I don’t know if I’ll be around 20 years! I may. But then I may not.

So why on God’s planet are insurers and the press allowed to quote ‘5% or whatever rate’ on this annuity? I don’t even know if I’m going to live long enough to get my money back, let alone make any money on the thing?

This is why, to answer my original question, we have to ask a very precise question – what is the internal rate of return (IRR hereafter)

Simply, the IRR is the rate of return that makes the net present value of all cash flows (what I paid in and the future stream of income I get back) from this particular investment equal to zero. In other words, it’s the rate at which my investment breaks even! The higher the IRR, the more attractive the investment. Since all I really know when I buy an annuity is how much they are going to pay me each year (£5,000 in our previous example) but not really for how long they will pay that money for, IRR helps me work out when or at what rate I start to make money.

So, what is the IRR of a typical annuity? Ehr… ehr … ehr… goodluck finding out! When you do, let me know.

Meet Mr Cazalet

Luckily for you, a very clever chap called Ned Cazalet did the maths in his recent 129 pages report titled ‘When I’m Sixty-Four‘ ( I kid you not, its 129 pages!!!). Mr Cazalet is a staunch critic of life insurers, who strangely manages to drum up so much consultancy work from them! You’ll think the insurance industry would hate him but no, they love the guy!

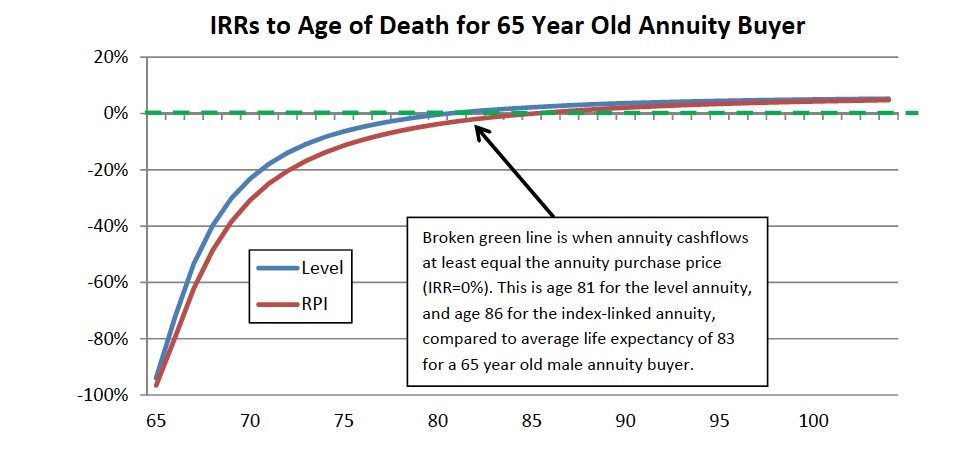

Anyway, so I pinched the graph below from page 71 of his report, which is based on a 65 year old male investing a £100K in a typical annuity.

To qoute Mr Cazalet…

‘For a level contract where the 65 annuity buyer dies after 5 years, the IRR is a woeful -30%. If the annuitant survives for 10 years (to age 75) the IRR is still negative at -8%, and if his death

matches his life expectancy (after 18 years at age 83), the IRR is a measly 1%. Even if he lives to be 100, the IRR does not quite reach 5%.’

OK, so based on average life expectancy, the IRR is 1%! So, explain to me again why lifecos, and their friends in the press quote annuity rates as 5%-6% etc when, on average life expectancy, you could just about expect to break even? Beats me!

Annuities Are Poor Value! Or Are They?

Am I saying annuities are poor value? I guess that depends on what you’re buying. One reason we love to hate our annuity is because we don’t really know if it’s an insurance or an investment. It tries to be both, but clearly not neither very well. This is nothing new of course, the insurance industry has a long track record of churning out products that tries to double up as an insurance and an investment. Endowments anyone?

If you think you are buying an insurance product, then really you should expect to lose money on average. You don’t really expect to make money on your life insurance, do you? You’ll be dead anyway! Nor do you expect to make money from your car or home insurance. You insure against a risk and the best you could hope for is for that event you’re insuring not to happen, in which case you happily ‘lose’ your premium. Accordingly, by buying an annuity, you are insuring against the risk of living too long. You’ll likely lose money but that’s the whole point. Based on law of average, 50% of people who buy an annuity will die before their life expectancy and they’ll lose money. The other 50% will survive, and make money but not much.

The problem is that people buying annuities are lead to believe that they are buying an ‘investment’ and they are expecting a decent ‘return’. Annuities are bad ‘investments’. They are supposed to be. They may be good insurance products, but they are bad investments. Don’t expect to make any money out of them.

This problem is exacerbated by the fact that we don’t really have a longevity insurance market in this country. Imagine I could buy a pure insurance policy to pay me a lump sum or an income if I live beyond my life expectancy at the point of buying it? Just the same we buy pure life insurance that pays a lump sum or an income for untimely death. Then we make a clear distinction between an investment and an insurance policy. Then people could buy a pure insurance product and accept they’ll lose money if the event they are insuring for doesn’t happen (only this time, that event may be desirable rather than adverse.) Then it’ll be a lot harder for annuity providers and sellers to pull the wool over our eyes! Not that they won’t try!

Read Full Bio

Annuities, I love this subject. If you ask me, they are an insurance product against living too long or becoming immortal and not having money to live on.

The product you are looking for is about to be launched based on the new pension flexibility legislated by the Pension Taxation Act 2014. It is named a deferred annuity. In one year you will be able to buy one from our insurance, although I do not think there will be too much demand for them. For example if you want to buy a pension annuity or a lump sum pension paid from age 82 onward, the insurer will be able to quote you. Obviously if you do not survive till then, you do not get nothing.

The IRR analyse does not have any relevance, as Critical A and B are not relevant either for choosing the alternative – pension drawdown. These are average returns or we know that in lifetime pension withdrawals the importance of investment return is insignificant comparing the sequence of investment returns.

Actuaries found this for the first time in 2003-2004. Then they were trying to pay some 10 years endowments and they found that although the fund has a 6% per annum investment return, the value to be paid was less than the premiums the clients paid into the product. They did not make much noise of it, they even paid more than the premiums, using reserves build in those with-profits funds between 1983 till 1999, but they realized the problem and the majority of the insurers closed the with-profits fund afterwards.

Insurer are just businesses which are governed by capital adequacy rules. They can take more risk and try to offer better annuities, but their need to hold capital will outweigh the profits as a result.

This is an important discussion to be had. We have a new possible option: Collective pension scheme. I am not sure these could add something better, but they can certain could ride better the sequence of investment returns.