We regularly get asked to look under the bonnet of products/providers and sometimes I find myself persuading advisers turn their back on products/providers they have recommended for some time – this can range from out-of-touch platform providers to poor value products from Dinosaur Life.

Anyway last week, it was the turn of MetLife Guaranteed/Income For Life Bonds. If you are familiar with product, you know that (ignoring the bells and whistles), it has a very simple promise – as long as client stays invested for a minimum of 10 years, they will get back their original capital back, less any withdrawals they have made, regardless of what happens to the stock market in that period.

For this privilege, the MetLife has a ‘guarantee charge’ which in addition to all the other product charges, pegs the TER (before adviser charge) on this Bond at something range from 2.3% – 2.9%pa! Can you please add typical adviser charge to that and let me know what you get?

So I put together an argument against this product and it goes something like this: – if the client is prepared to stay in the market for 10 years (and in this case, possibly longer) we don’t need to pay 2.9%pa for capital guarantees because the market, in a way, already offers that.

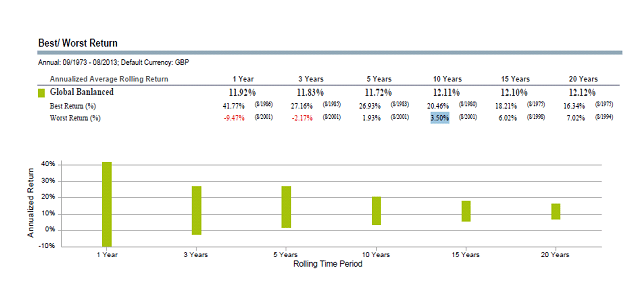

To proof my point, I back-tested simple 50/50 portfolio with global asset allocation (50% MSCI World and 50% in Dimensional Global Fixed Income Index) over the last 40 years – the longest period available and this is the result.

The worse performance over ANY 10 year period is 3.50%pa. In order words, ignoring inflation and fees, there has been no full 10 year period with a negative return or capital loss on this portfolio over the last 40 years.

So can anyone please explain to me why I should pay MetLife 2.3%pa to get something the market has given? Last I checked, the TER on our typical evidenced-based portfolios is 30pbs!

OK, you can accuse me of predicting future returns based on past performance. And off course the market offers no explicit guarantee on capital. My point is, we invest in the markets because there is an established pattern of behaviour over the long term. And don’t forget that this pattern has been tried and tested by some of the most brutal occurrences in living memory including the dot-com bubble, terrorist attacks and Credit Crunch.

I think it is reasonable to project our expectation based on something tried and tested. But if we can’t trust the market – the foundation upon which our economy is built, why on earth should we trust MetLife or any other provider for that matter?

Then I dug into MetLife’s portfolios offered to clients investing in the guaranteed bond. The Managed Wealth Portfolio Min for instance, has at least 80% invested in index trackers! (oh and did I mention there are future contracts in there too?)

It appears to me that MetLife is well aware of this fact that the market does offer some in-built protection to long term investors anyway but by making that protection explicit, it can effectively make bucket load of money at the expense of unsuspecting investors (and advisers?)

Off course, I have made the schoolboy error of classical finance theory here; I assumed that the client is going to stay invested for the next 10 years but in actual fact, the bumpy ride along that journey probably means they won’t. Behavioural finance expert might argue that the knowledge of explicit guarantee on their capital after 10 years is a useful tool to keep client invested for the full term. This is true but my only push back is how much is that emotional insurance worth? And isn’t that a big part of why clients hire an adviser; someone is going to hold their hands through the journey, especially when the going gets though? So if client is paying an adviser for that emotional comfort, surely they don’t need to pay MetLife or anyone else? Or is it the other way round?

Read Full Bio

Yep, using Met Life is literally akin to burning £10 notes in front of your clients face, laughing and then running off with his wife.

That made me laugh. Finally found something you and I both agree on… Yippee! Success!

That is a FANTASTIC piece. Abraham. You’ve nailed it.

Thanks Nick!

Very well said Abraham. One of the few things we, as advisers can influence, is how much it costs our clients to invest their money. 2.9% pa of anyone’s money is too much, partularly with the low level of risk presented.

The idea of Metlife’s contract and contracts of this type is always very appealing in that it gives a guarantee that we can’t, BUT everytime I look at the Metlfie contracts I come to the conclusion like Abraham, that the cost of the guarantee wipes out any benefit of having it in the first place. AEGON’s 5forLife and The Hartford’s GRIP (5% for life on pensions) did have a logic to them I could accept and felt able to reccomend to clients as an alternative to an annuity or standard no guaragtee drawdown and becuase Purchased Life annuities just aren’t competitive, but Metlife’s contract?

I agree Abraham, I still don’t think it’s worth the money, a bit like asteroid insurance….. yes, it may happen, but if it does we’re ALL Fxxxxxx anyway.

Thanks for your comments Phil. I like you conclusion…. couldn’t have said it any better.

We have examined this product many times and found it to be expensive, however I think you have missed a point and that is around mortality risk, what this product also does is guarantee an income stream for life, in that sense it has charateristics of an annuity but without the permanence. I don’t work for Met Life but have frequently had to compare them against our own much better and cheaper investment products. This is missing the point and we usually lose as it is pitched as a solution to a different customer need. It used to pay big commission pre RDR and suspect it will go the same way as the much better value 5 for Life & Hartford products now.

I haven’t used any plans with explicit investment guarantees for sometime now so wondered which if any the posters think are value for money?

The reason why I use explicit as a word is I have used MGM’s Flexible Income annuity which has an implicit minimum income built in and benefits from mortality subsidy and gives access to both Vanguard Passives and Jupiter Merlin Funds which I think are suitable for mass market use at a fair price

I’d be interested to try this with the Aegon Unit Linked Guaranteed investments. What services do you use to compile back testing?