Target Date Funds are becoming increasingly popular in the UK. The UK market is still very small (only around 0.5% of the DC market) but its expected to top £10 billion by 2018, with products such as BlackRock LifePath, State Street Timewise and Alliance Bernstein’s Retirement Strategies, becoming default options ifor DC investors, and JPM SmartRetirement and Architas BirthStar (managed by AllianceBernstein) launched in the advisory and D2C channels. We know that a few other providers are to follow.

WTF is TDF?

Technically speaking, TDFs are simply investment strategies based on the date a sperm fertilizes an egg! 🙂

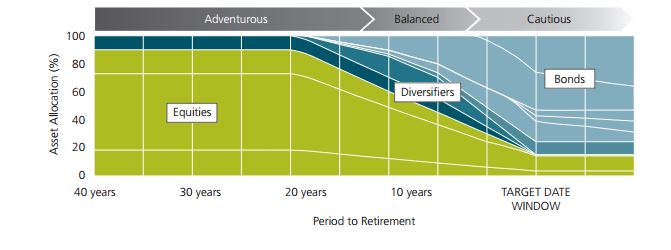

Okay, seriously… TDFs (also called life-cycle funds or age-based funds) put asset-allocation on autopilot-based client’s age or more specifically, the time they have left before reaching their retirement age. Younger investors start out with high allocation to equities (and other growth assets) and this reduced gradually, while the fixed income (and other defensive assets) allocation increases proportionately as they approach that important retirement date. The typical asset allocation glide path will start at 80/20 stock/bond allocation and move gradually over time to 20/80 equity/bond allocation. This chart below shows a typical asset allocation glide path for TDFs.

Image from Alliance Bernstein

The idea behind TDFs appears very intuitive; younger investors have longer time to recoup losses, than older clients who are closer to retirement and haven’t really got time for portfolio to recover before having to draw income – but does it really stand up to scrutiny?

Do TDFs stack up?

Do we really think that younger investors, with very little or no investment experience and probably very little by the way other assets should allocate 90% of their portfolios into equities? TDFs take no account of the investor’s risk profile or behavioral biases and so when craps hits the fans, what’s to stop these folks from panic-selling and sitting on cash? And worse, they become scared of going back into equities. While the idea of high equity allocation for younger investors makes sense, it fails to account for the behavioral biases that has been known to have significant influence on investment outcome.

Behavioural biases aside, TDFs also result in suboptimal outcomes in terms of capital accumulation and by implication, retirement income. TDFs automatically allocates clients to defensive assets at the time when the probably have the highest account balances, reducing the overall growth in their portfolio when it’s most needed. In other words, when investors have very little money (to make returns on), we load them up on growth assets and when they actually have a decent-sized pot, we gradually take risk (and hence return) off the table.

Studies carried out by folks at Research Affiliates shows that doing the exact opposite of what TDFs do – i. e a rising equity glide path that starts out with low equity allocation (say 20% equity and 80% bonds) and increases as investor approaches retirement (say to 80/20 equity bond allocation) – or in fact, a the good old static 60/40 portfolio rebalanced Regularly – delivered better outcomes that the typical TDF glide path. In summary, their conclusion is that;

Markets don’t care about our glidepath (or lack thereof); we’re as likely to have our best stock market returns late in our career as early. If the best stock market returns come early, it’s clear that we’ll finish richer with a glidepath strategy. But if bonds beat stocks late in our career, we’ll do materially worse with a glidepath approach.

Having higher returns when our portfolio is large is important; over most historical spans, this means that finishing with an equity-centric asset mix trumps the classic glidepath strategy.

Their research is corroborated by Jarvier Estrada of EISE , whose comprehensive study that spans more 19 countries, and 110 years shows that when compared to TDF strategy, reverse glide path strategies (i.e increasing equity allocation as investor gets older) provides higher upside potential and more limited downside potential. In his words;

First, the mean and median terminal wealth are lower with strategies that become more conservative as retirement approaches (lifecycle strategies) than with those that become more aggressive as retirement approaches (contrarian strategies). Second, contrarian strategies outperform lifecycle strategies in terms of all the upside potential variables considered here.

Third, contrarian strategies keep investors more uncertain about their terminal wealth than lifecycle strategies. But, fourth, the former’s downside potential is typically more limited; that is, contrarian strategies tend to deliver a higher terminal wealth in bad scenarios than lifecycle strategies do. These last two points combined imply that, fifth, the higher uncertainty of contrarian strategies is basically uncertainty about how much better, not how much worse, investors are expected to fare with them than with life-cycle strategies.

The point here isn’t necessarily to suggest that increasing equity allocation as an investor gets older is always the right approach but more to demonstrate to folly of TDFs and the conventional view that asset allocation should become more conservative as people get older, regardless of their risk profile and whatever else going on in their lives.

With Pension Freedoms, we know that more and more people going into drawdown rather than buying an annuity, I find the idea of putting clients in 70%/80% defensive asset at the start of what is likely to be a 30 year plus retirement period worrying indeed. Strangely, Pension Freedoms is being seen as an opportunity to flog more of these products in the retail and advisory channels, and TDFs are replacing lifestyling as the default options for millions of DC savers. I fear we are heading in the completely wrong direction and I can only hope someone stops this madness before it’s too late! Then again, I’m totally used to being told I have no idea what I’m talking about, so here’s your chance to show me empirical evidence that I’m wrong. What am I missing?

He holds a Master’s degree from Coventry University and an alphabet soup of qualifications, including the Investment Management Certificate, Chartered Financial Planner, CFP and Chartered Wealth Manager designations. He was one of 5 finalists for the Professional Advisers Personality of Year Award 2015 but the award went to a more deserving winner, obviously!

Read Full Bio

First I will start that the majority of the TDFs should not be based on the employees’ date of birth, but on the expected retirement age for the employee. Obviously with young employees this will be a bit of guess or and educated guess – using their SPA age if nothing else. Nest uses this approach – “We expect most NEST members will invest their money in the NEST Retirement Date Fund that matches their planned retirement date.”.

We do not know what retirees will do in the next 20 years and I believe that it is too early to say that they will buy a pension annuity, or they will encash it and spend it one go, or they will use it for pension withdrawal. I am looking at the Australian experience and it seems that 15% buy annuities, 20% cash it immediately to repay mortgages and debts, 40% use the fund for pension withdrawals, but exhaust the fund over a period of 3 to 10 years (to take the advantage of a means tested Old Age pension) and about 25% used it to lifetime income.

It is not hard to realize that the last 25% are a lot more wealthy people who have a financial adviser that advises them on which fund to use within the DC pension scheme and as a result they do not use TDF funds when closer to retirement. So I suppose, if these funds are not going to be used for people looking for a lifetime income in retirement, they should not be designed from the beginning with this in mind!

As a result they should help the other two categories: have an option for people who buy a pension annuity – so at their retirement age the fund should be in long duration gilts and bonds. This could be named “deferred annuity” option and another option for people who need to fully cash the pension fund and/or retirement income for a short period of time – the asset allocation could be 50% cash and 50% short duration bonds at their retirement age.

I do get to review a lot of DC pension plans and have seen all the BlackRock Aquila funds (which are most used) and my empirical research resulted that the best outcome for the last 15 years was 75% equity/25% bonds. I am not saying this will be the best asset allocation for the next 15 years. By best outcome, I mean in this case highest fund. You get the same result using the latest 15 years data into a efficient frontier calculator as well.

Efficient frontier calculator are good when you use past data to get which strategy have performed better in the past. Unfortunately they are not so good for the future, mainly because the calculations will be fraud as a result of too many wrong assumptions you could make: investment returns, standard variations and correlations etc. I always said that making assumption for these data could throw you well of the mark and if someone wants to play I will email you my spreadsheet to have a go – the highest performing portfolio in the next 20 years could be anything between 30% equity/70% bonds and 100% equity. As I always say you put garbage in, you should not expect anything than GARBAGE out i.e. the GARBAGE principle.

I did stop to the efficient frontier of optimal risky portfolios because the Australians did something amazing, the took the modern finance theory to a new level – they introduced GEARING into DC pension funds. The results were very good in the last 20 years, following what the modern finance theory predicted – the return of the portfolio will be higher, a lot higher and I had the pleasure to review a few Superannuation funds that use gearing myself.

The gliding path used by life-cycle funds is based on risk capacity, not on maximizing investment return. Here there is the important definition that people involved in finance forgets (myself I have a background in rocket science and ammunition so I don’t) risk definition is probability multiplied with SEVERITY. People could google it if they do not believe me.

So even after you do the Monte Carlo simulation and you get the probability of 1% for someone to run out of money in retirement, the SEVERITY of that event is huge resulting in a high risk approach which should be avoided. As Paul Armson nicely puts it “In life there is no rehearsal”. However I need now to use the GARBAGE principle: “garbage in, garbage out”. So if I play a bit with your assumptions (change the normal distribution into a leptokurtic distribution, increase the inflation and volatility by a notch) what was 1% probability event could become 10-15% probability event. If I tell you now to go out driving the car telling you have a 10%-15% probability of dying, you would not do it. Why you will not go out driving, because it is TOO RISKY.

The FCA was good in introducing the capacity for loss (risk capacity) into the equation as a measure of risk and sanity. If was the first time when the regulator asked us to look at the severity of our actions.

I believe that recommending a pension fund that works on a increasing equity exposure as the employee gets older to an employer into their DC pension scheme is a high reputation risk for the employee benefit consultant firm and none will take this risk. Some things will just not take off of the ground (in rocket science speak).

Going back to behavioral investing, it seems that NEST thinks it is better not to start young people on a high equity allocation as they can get scared and opt out of the scheme altogether. As a result NEST reduces the equity allocation for young people in some of the funds targeted to them. From my empirical research, this seems not to be true. I have very cautious clients and I found them in DC pensions in use or deferred having 80%-100% equity allocation. They do not get scared mainly because they do not look too often at their pension plan value (probably the are too busy looking to find beautiful men and women) and when I asked they told me they did not become aware that at one time (2009 March) their pension fund was nearly 45-50% down. I may not be right and I remain open to other opinions.

Going back to TDFs, it is hard to know which the optimal solution will be, especially now that the Government is consulting into moving into TEE (taxed, exempt, exempt) pension system. If they do, they pension contributions would need to be compulsory as in Australia, because otherwise people will opt out if there is no tax relief given.

In the end, the Government will need to get rid of NICs and combine them into the income tax rates and introduce a means tested State pension. The Conservative Government is looking into getting rid of NICs, but they will need courage to change the State pension to a means tested system. However the demography is not forgiving, so one day it will happen. There are countries already who have more retired people than working and to cope with this you need a means tested State pension system. As an example, China has built its new pension system on a TEE system combined with means testing as it expects a big demographic problem in 30 years.