case studies

Included case studies presented in a simple, clear and concise way that clients can relate with.

DESIGNED FOR ADVISERs

Advisers can download the guide, add their logo to the front page and share with their clients.

completely free

There’s no charge for using this guide. Consider it our labour of love.

Thanks for stopping by!

We’re excited to share our FREE Guide to sustainable retirement income for advised clients.

Many factors contribute to a successful retirement; figuring what you’re going to do with your time, keeping physically and mentally active, and managing your financial resources in a way that helps you achieve what matters to you. This guide is dedicated to the financial aspect – specifically, how to make sure your retirement portfolio lasts for as long as you need.

The Big Retirement Question

This is what Nobel Prize winner William Sharpe calls the single ‘nastiest, hardest problem in finance.’ Sharpe should know – he’s an 84-year-old retired professor of finance from Stanford University, Nobel Prize winner and has an investment metric (the Sharpe Ratio) named after him.

This guide is designed to help advisers communicate the specific risks associated with drawing income from a retirement portfolio and how to make sure the money lasts a lifetime.

[bctt tweet=”Managing withdrawals is a delicate balancing act, thanks to the complex and nuanced nature of mitigating sequence and longevity risk. ” username=”AbrahamOnMoney”]

Designed for advisers to use with their clients

Retirement planning is akin to mountaineering in many ways. Accumulating your savings is the ascent and spending them is the descent. Financial planners are like mountain guides – financial Sherpas if you like. We believe that everyone benefits from having a retirement Sherpa, a financial planner who applies robust and empirical evidence to retirement income planning.

Accordingly, we’ve designed the guide with financial advisers and their clients in mind.

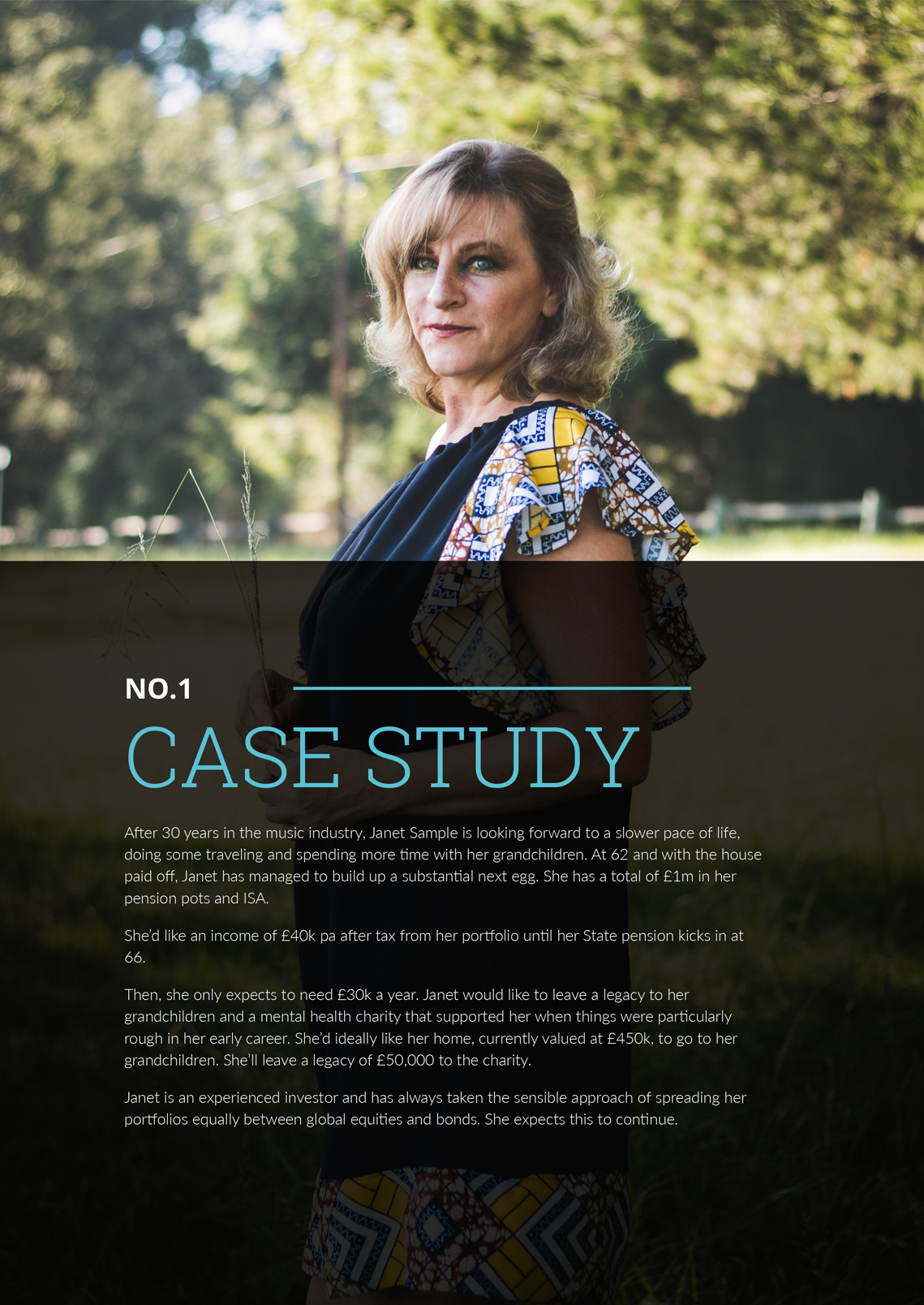

Case Study 1

Janet Sample

After 30 years in the music industry, Janet Sample is looking forward to a slower pace of life, doing some traveling and spending more time with her grandchildren. At 62 and with the house paid off, Janet has a total of £1m in her pension pots and ISA. She’d like an income of £40k pa after tax from her portfolio until her State pension kicks in at 66. Then, she only expects to need £30k a year. Janet would like to leave a legacy to her grandchildren and a mental health charity.

Policy Statement

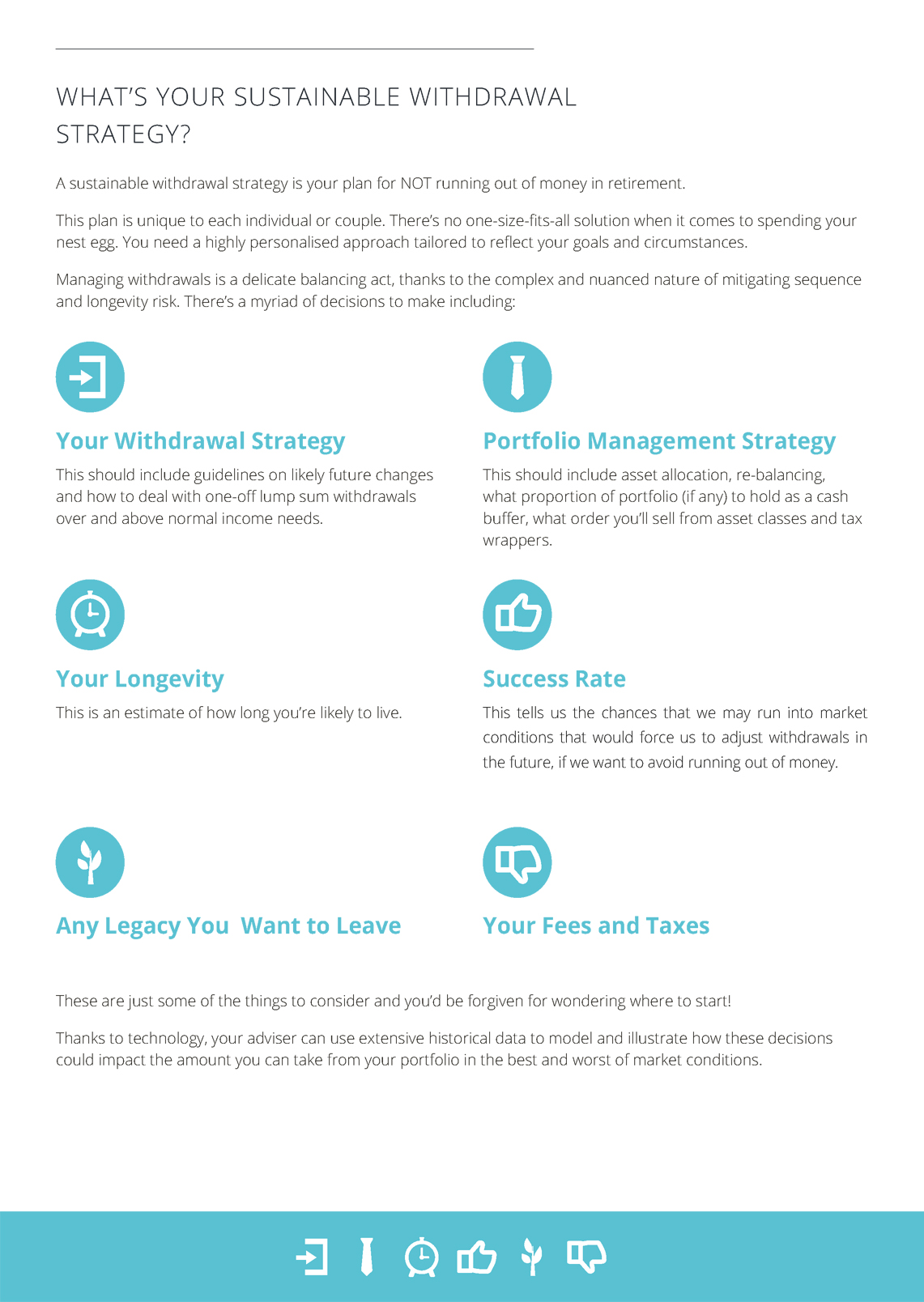

Your Strategy

Managing withdrawals is a delicate balancing act, thanks to the complex and nuanced nature of mitigating sequence and longevity risk. This plan is unique to each individual or couple. There’s no one-size-fits-all solution when it comes to spending your nest egg. You need a highly personalised approach tailored to reflect your goals and circumstances.

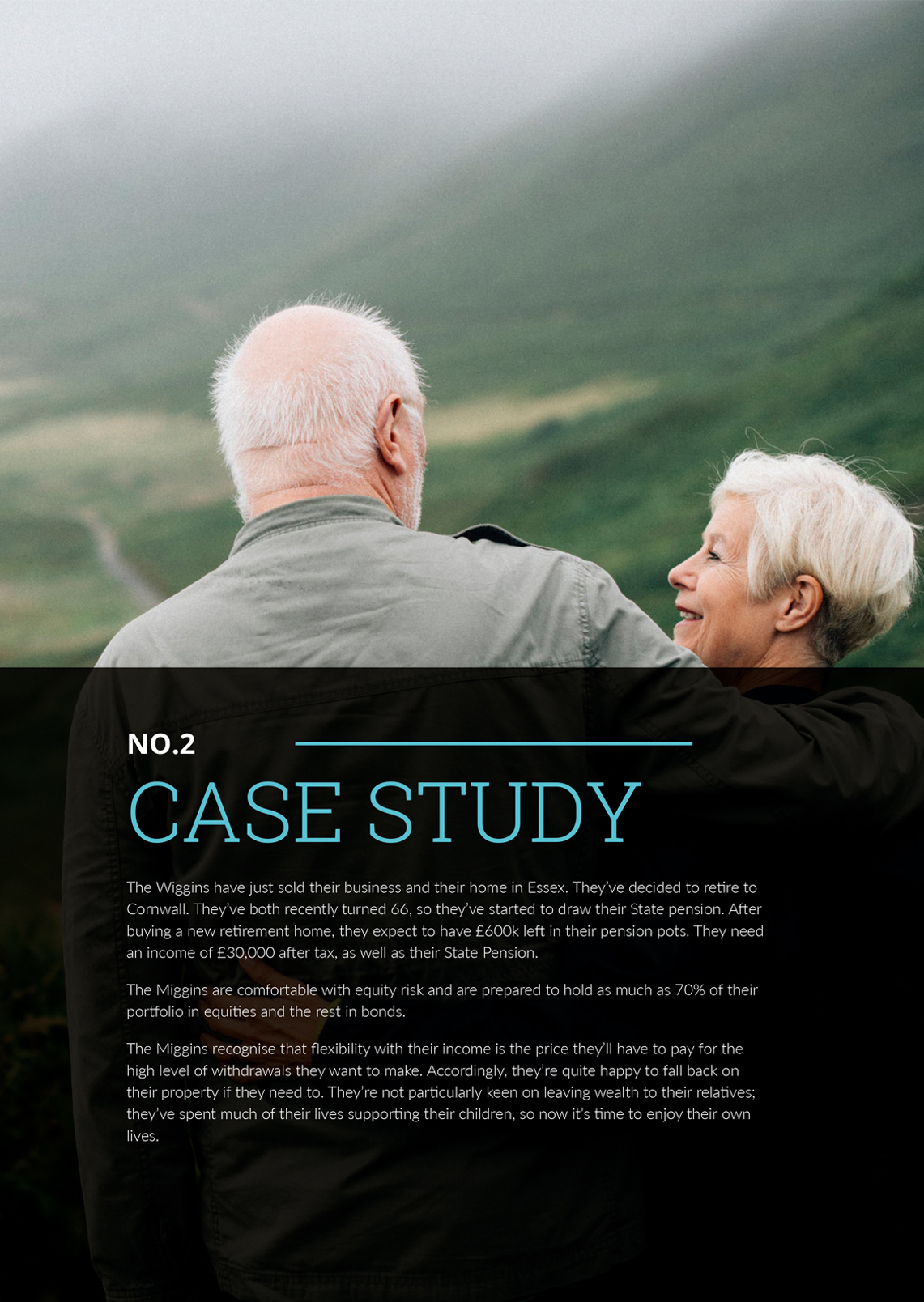

Case Study 2

Jake & Jo Miggins

The Miggins have just sold their business and their home in Essex. They’ve decided to retire to Cornwall. They’ve both recently turned 66, so they’ve started to draw their State pension. After buying a new retirement home, they expect to have £600k left in their pension pots. They need an income of £30,000 after tax, as well as their State Pension. They’re not particularly keen on leaving wealth to their relatives; they’ve spent much of their lives supporting their children, so now it’s time to enjoy their own lives.

ready to go?

By downloading this guide, you agree to our terms of use which are set out below

Terms of use

- All rights reserved. This material is reproduced under license by Timelineapp Tech Limited.

- This guide is designed only for use by financial advisers, authorised and regulated by the FCA. If you are not an FCA-authorised financial adviser, please contact us. Downloading this document without the appropriate FCA authorisation and/or our express written permission, is a breach of our intellectual property – that is a theft.

- We grant authorised financial advisers the permission to add their logo to the front and back cover of this guide. No further changes can be made to this material without written permission.

- The content is for educational and illustrative purposes only. Nothing in this document constitutes investment advice and must not be relied on as such. The value of investments and the income from them can go down as well as up. You may get back less than you invest. Past performance is not a guide to what might happen in the future. Transaction costs, taxes and inflation reduce investment returns.

- It is entirely up to the adviser to seek and obtain permission from their compliance to use this material with clients. We can not get involved in that process in any way.